Received: 12th November 2022 Review: 25th January 2023 Accepted: 3rd Marach 2023

Abstract Purpose

This study aims to examine the impact of board qualities on the financial performance and asset quality of new private banks.

Design/Methodology/Approach

Fixed-effect robust panel data regression analysis is used based on the Hausman specification test and the Breusch-Pagan Lagrange multiplier (LM) test. A sample of 7 new private sector banks operating in India from 2011 to 2020 is evaluated for the study. Data on board characteristics are acquired via annual reports and the “Centre for Monitoring the Indian Economy’s prowess database” is used to collect data on financial performance, asset quality, and control variables.

Findings

We found that the proportion of independent directors, female directors, board commit- tees, and meetings have a significant impact on the return on assets. Regarding asset quality, along with the above four characteristics, the average no. of meetings attended and non-executive directors have a significant impact on gross non-performing assets.

Practical Implications

Banking activities are comparatively complex and opaque. Furthermore, the role of top management in recent banking problems emphasizes the importance of conduct- ing the study. This research will strengthen the understanding of the implications of board characteristics among researchers, investors, and policymakers.

Originality/Value

Previous research works studied all banks, but new private banks vary from old pri- vate banks and public banks in terms of governance, as they are different on the grounds of structural dissimilarity and reporting differences. So, we only considered new private banks in our study.

Keywords: Asset quality, Return on the asset, Board of directors, Corporate gover- nance

http://doi.org/10.53908/NMMR.310104

- Introduction:

Corporate governance has long been credited with ensuring a company’s success in the marketplace. When many issues, such as Enron, WorldCom, Parmalat, or Lehm- an Brothers, came to light, the importance of strong corporate governance was felt worldwide. The growing size and complexity of India’s financial sector underline the value of improving bank governance standards. Recent banking problems have also raised new concerns about the effectiveness of Indian banks’ corporate governance. A large number of studies have been conducted to investigate the effect of governance practices on firm profitability. However, in India, the surge in corporate governance research has only occurred in the last decade. Mandatory regulations, listing agree- ments, and improved governance norms have all aided the growth of governance research in India.

The nature of banking activities is comparatively complex and opaque. Hence it is challenging for the creditors, shareholders, debtholders, and regulators to monitor the bank. In comparison to non-financial enterprises, banks are associated with additional asymmetric information (Andres & Vallelado, 2008). Banks made long-term ties with clients to mitigate the informational asymmetry problems. Also, the depositors are not financially literate to understand the complexities of banking activities. Owing to opaqueness, insiders have more opportunities to exploit stakeholders (Levine, 2003). Banks have more leverage on their financial statements and, on average, more debt in the form of deposits than other businesses. Customers are granted loans from these deposits, which usually have long maturities. In this way, banks maintain liquidity in the market by retaining illiquid assets and releasing liquid liabilities (Macey and O’Hara, 2003). Sometimes top management of banks also gets involved in scrupulous activities like diverting funds to themselves or shadow companies, further leading to an increase in non-performing loans. It emphasizes the responsibility of directors to oversee operations honestly and transparently. As per convention, private banks in India have been classified into two categories new and old private banks. They are differentiated on the grounds of structural dissimi- larity and reporting differences. Old banks ran for over half a century and didn’t get nationalized by the government. On the other hand, new banks the ones that came in the early 1990s. Also, new private sector banks are comparatively larger in both size and scope, so special attention is required to understand the influence of governance on these banks’ asset quality and financial performance. The majority of empirical research on the relationship between private bank board governance and performance has been conducted in developed countries. Most empirical work connecting the board governance of private banks to performance is covered in developed countries. Private banks’ relevance and contribution to the overall banking sector have grown over the last two decades The unique characteristics of financial intermediation and the spillover impact of governance failures made this study crucial to research. This study is an initial attempt to examine the role of board dynamics in new private banks, which account for a sizable portion of the private banking group. We work on the fol- lowing research questions:

- Are board characteristics and performance related to each other?

- What are the primary board characteristics that influence private banks’ asset quality and financial performance?

Data on board characteristics are gathered manually from annual reports published by banks. The “Centre for Monitoring the Indian Economy’s prowess database” is used to gather information on financial performance, asset quality, and control variables. To achieve the research goal, we use the Fixed-effect panel data approach on the balanced dataset. Researchers, investors, and policymakers, we believe, will acquire a better awareness of the impact of board traits in the banking industry. It will also direct them to concentrate on certain board traits relevant to private lenders, which significantly impact profitability and asset quality.

In the following sections of the paper: In Section 2 hypothesis are framed based on the literature review, and Section 3 discusses the sample, data sources, models, and discussion of empirical results. Section 4 concludes and provides the future scope of study.

2. Literature review and hypothesis formulation

Firm ownership and control are the two different things that act as significant con- tributors to conflicts between owners and controllers. Jensen and Meckling (1976) have formulated the agency theory based on the same concept. So, controllers are those people who actively work on behalf of the shareholders (owners) therefore an effective mechanism to control the managers needs to be ensured (Fama and Jensen, 1983). The responsibility of monitoring the managers is entrusted to the shoulders of the board of directors, who are agents appointed by the principles. Moreover, they also act as advisors in designing effective policies and strategies as per their mission and vision. According to Gillan & Starks (2003), the cost and benefit of the monitor- ing mechanism differ substantially across industries, so corporate governance struc- tures are also different across industries and firms. The banking industry is quite dif- ferent from other sectors as it is the most regulated industry. The government keeps a close eye on the banks, owing to the role they play in the economy (Renee B. Adams & Mehran, 2003).

Corporate governance has a favorable impact on the organization’s long-term viabil- ity and profitability. Various studies have put a lot of effort to study the influence of governance mechanisms. For example, firms with superior governance systems report that the board has a favorable impact on the firm’s financial performance (Ad- ams & Mehran, 2012; Almoneef & Samontaray, 2019; Mayur & Saravanan, 2017). By balancing non-financial and financial goals, organizations with a strong board of directors report increased profitability(Lafuente et al., 2019; Polovina & Peasnell, 2015) and produce more excellent business value, improve market liquidity, and pay higher dividends and bank yield (Battaglia & Gallo, 2015; Bokpin, 2013; Ondigo, 2019; Safiullah & Shamsuddin, 2019; Tanna et al., 2011). Also, Board positivelyinflu- encesthe bank’s risk-taking strategy (Ben Zeineb & Mensi, 2018; Dong et al., 2017; Pathan, 2009).

The global financial crisis was the banking industry’s turning point, though India was least affected by it. Regulators and academicians observe the importance of gov- ernance and contribution to financial and non-financial performance. Based on the study of 34 commercial banks in India, Battaglia et al. (2014) found that the charac- teristics of the board play a prominent role in the bank’s governance. Handa (2018) determine what effect board arrangements have on financial performance from 2008 to 2015. She claims that the following factors CEO duality, average salary, board committees, and female participation all have an impact on bank performance. Dey & Sharma (2021) also suggesteda negative connection between Board size, Board meet- ings, board committees, and board independence and the financial performance of public sector banks.At the same time, the relationship between women directors, non- executive directors, and executives is favorable. Based on the study of 35 scheduled commercial banks over seven years, Jaswal & Aggarwal (2021) concludes that board governance has mix impact on ROA and ROE. Some variables as no. of the board meeting and board independence affect negatively while board size affects positively. The body of literature suggests that board characteristics have an impact on perfor- mance (Bezawada, 2020; Handa, 2018;Sarkar & Sarkar, 2018; Jaswal & Aggarwal, 2021; Aqlan et al., 2020; Abdul Gafoor et al., 2018; Mayur & Saravanan, 2017; Kanojia & Priya, 2016).

Jadah et al., (2016) worked on an unbalanced panel dataset related to 20 Iraqi banks from 2005 up to 2014. Various authors report that the characteristics of the board have a positive effect on return on equity. Pathan et al. (2007) examined thirteen Thai banks from 1999 to 2003 and find that board features have a detrimental effect on bank per- formance. Liang et al. (2013) found that board features have a detrimental effect on financial performance indicators in thestudy of the 50 largest Chinese banks from 2003 to 2010. Results from a sample of significant European banks that obtained rescue pack- ages, Fernandes (2016) claimed that the qualities of the board have a major effect on the stability of banks. While El-Masry (2016) discovered that board features of con- ventional banks have no impact on performance, the outcomes for the Islamic bank-ing system turned out to be unfavorable. Numerous studies looked at the connection between bank performance in developed countries and board characteristics. ( Andres & Vallelado, 2008; Belkhir, 2009; Berger et al., 2014; Bertay et al., 2013; Ferreira et al., 2012; Haan & Vlahu, n.d.; Lin & Zhang, 2009; Mehran, 2005;Nyamongo & Temesgen, 2013; Pathan et al., 2007; Pathan, 2009;Renee B. Adams &) and specifically in India (Abdul Gafoor et al., 2018; Aqlan et al., 2020; Bezawada, 2020; Dey & Sharma, 2021; Handa, 2018, 2020; Jaswal & Aggarwal, 2021; Kanojia & Priya, 2016; Mayur & Sara- vanan, 2017; Sarkar & Sarkar, 2018). Surprisingly, some researchers contend that board specifications have little bearing on bank performance. (Laeven, 2013). So, we can infer that the literature on corporate governance in banks did not provide convincing findings on the effect of board governance on the performance of banks. According to one school of thought, board efficiency reduces conflicts of interest and successfully addresses the principal-agent problem. Others argue that there is no discernible effect.

Several studies looked into the inter-relationship between board governance and the performance of commercial banks. In most of the studies, all banks are considered in a single sample. In line with the government’s bifurcation, private banks can be further classified as old private banks and new private banks. Even Nayak (2014) has demonstrated that the board structure and practices of both banks vary from each other which affects strategic decision-making in the organization. To the best of the author’s knowledge, few studies have explicitly worked on new private banks, so considering this a novel area, the purpose of this study is to shed light on how board composition can influence profitability and credit risk-taking in the context of new private banks in India. For empirical testing, the study suggests the following alter- nate hypothesis.:

- Hα1: Number of the directors on the board has a substantial impact on the bank›s performance and asset quality.

- Hα2: The impact of non-executive directors on banks› performance and asset qual- ity is significant.

- Hα3: The number of independent directors on a bank›s board substantially impacts its performance and asset quality.

- Hα4: Level of female participation has an impact on bank performance and asset quality

- Hα5: The number of board committees has a significant influence on performance and asset quality

- Hα6: The number of board meetings has a significant influence on performance and asset quality

- Hα7: Board of directors diligence represented by attendance ratio in the meetings has a significant impact on bank performance and asset

3. Research design

3.1 Data

The study is a preliminary work to examine the influence of different board qualities on asset quality and performance of new private sector banksWe intended to work with a sample of ten banks, however, in the final selection, seven banks are evaluated based on data availability across research variables and temporal dimensions. The data is based on balanced panel data from 2011 to 2020, with 70 bank-year observa- tions. The gross non-performing asset proportion is used as a proxy for bank asset quality, and the return on asset is used to gauge bank performance. Because the size of a company and the tenure of a bank have an impact on its performance, we use them as control variables to limit the impact on dependent variables. The data for response variables and control variables were extracted from CMIE Prowess, the Centre for Monitoring the Indian Economy’s database. The CMIE database is an authorized source of information (Arora & Sharma, 2016), and provides monetary and financial information. The data for the explanatory variable is gathered manually from annual reports available on the bank’s website. Details of variables are:

| Variables | Description |

| Board size (B_Size) | The Total number of directors on the board in the respective financial year |

| Non- Executive director (NEx_D) | The ratio of outside directors to the board size in the bank |

| Independent director (Ind_D) | The fraction of independent directors on the bank’s board |

| Female director (Fe_D) | The fraction of female directors working on the bank’s board |

| Board committee(B_Comm) | Over the year, the total number of board committees exists in the bank |

| Board meetings(B-Mee) | Total number of regular board meetings held in the given financial year |

| Average attendance of director (Avg_Att) | The portion of independent directors who attended the annual general meeting to the overall number of independent directors. |

| Average no of the meeting attended (Avg_MeeNo) | The sum of board meetings should be attended in relation to the board size. |

| Return on asset (ROA) | Net Income earned in a financial year divided by Average Asset held by the bank |

| Gross non-performing asset (GNPA) | The bank’s gross non-performing assets as a share of total loans and advances in the financial year |

| Bank age (B_Age) | Total number of years since the bank’s inception |

| Bank size (logB_Size) | Natural log of the total asset |

Table 1: Variable’s name and descriptions

3.2 Empirical results and discussions

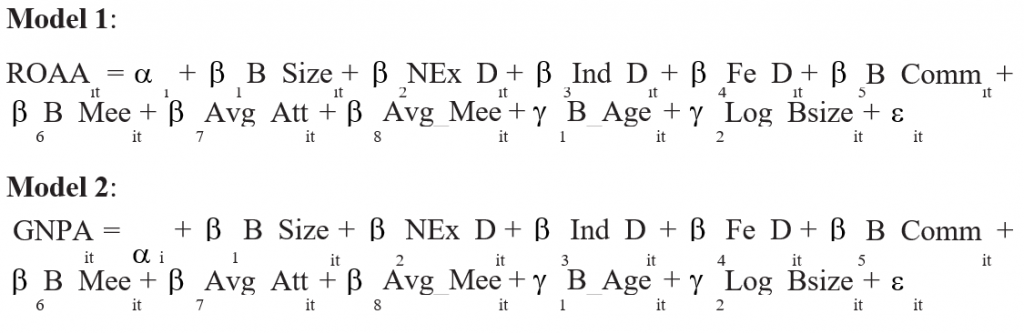

Panel data are observations from multiple periods about the same entity. We have data on the bank’s board of directors going back ten years, therefore we performed panel data analysis. Because we have consistent data over time, the data is balanced panel data. More meaningful data, more variety, less collinearity across variables, greater degrees of freedom, and even more efficiency are all benefits of panel data (Baltagi & Song, 2006). It also helps to control unobserved heterogeneity and endogeneity problems that arise because of omitted variables and measurement errors (Sarafidis & Wansbeek, 2021). Different methods can be used for panel data analysis as Pooled “Ordinary Least Square”, “Fixed effect”, and “Random effect”. Based on the Haus- man specification test and Breusch- Pagan Lagrange multiplier (LM) test fixed-effect method is used for panel data analysis. The fixed effect model is called fixed because the model intercept can differ across the different banks, but the bank-specific inter- cept is time-invariant. Econometric models used in the study are:

3.2.1 Descriptive statistics

In table 2, the descriptive characteristic of all the variables is summarized to under- stand the overall pattern and behavior of banks. The average number of directors is

10. For some of the bank’s board size is very large, 15 compared to 7 in some banks. The mean percentage of NEx_D and Ind_D is relatively high at 78 percent and 58 percent, respectively. Standard deviation is also very high in both dimensions show- ing high variability in non-executive directors and independent directors. The mean proportion of female directors’ 12 percent is relatively satisfactory. Banks have a sig- nificant tendency to have a large number of board committees, with an average of 11 committees. The average board meeting count per year is eight, which is more than the legal requirement. Skewness and kurtosis are the measures of checking the nor- mality of the data. Board size, Non-executive directors, female directors, number of board committees, and log of the bank assets have kurtosis value less than 3 (lighter tails than normal distribution) as compared to Independent directors, Board meeting, Independent director’s attendance rate, Average number of the meeting attended, re- turn on asset, Gross non-performing asset ratio, bank size, and bank age have value more than 3 (higher tails than to normal distribution).

| Variables | Obs | Mean | Std. Dev. | Min | Max | Skew. | Kurt. |

| B Size | 70 | 10.771 | 2.093 | 7 | 15 | .058 | 2.172 |

| NEx D | 70 | 78.636 | 10.334 | 58.333 | 92.308 | -.275 | 1.799 |

| Ind D | 70 | 57.924 | 14.094 | 0 | 92.308 | -1.457 | 9.722 |

| Fe D | 70 | 12.557 | 6.951 | 0 | 26.667 | .051 | 2.573 |

| B Comm | 70 | 11.329 | 1.567 | 8 | 14 | -.396 | 2.457 |

| B Mee | 70 | 8.757 | 3.453 | 4 | 20 | 1.319 | 4.728 |

| Avg Att | 70 | .885 | .076 | .655 | 1 | -.914 | 3.72 |

| Avg Mee | 70 | 6.751 | 2.758 | 2.818 | 16.444 | 1.593 | 5.838 |

| ROAA | 70 | 1.328 | 1.012 | -5.39 | 2.02 | -4.592 | 29.545 |

| GNPA | 70 | 2.767 | 3.005 | .2 | 16.8 | 2.907 | 12.529 |

| B Age | 70 | 22.5 | 5.669 | 9 | 36 | 0 | 3.144 |

| log Bsize | 70 | 14.644 | 1.298 | 11.372 | 16.676 | -.72 | 2.759 |

Table 2. Descriptive statistics for Independent, Dependent, and Control variables

3.2.1 Correlation analysis:

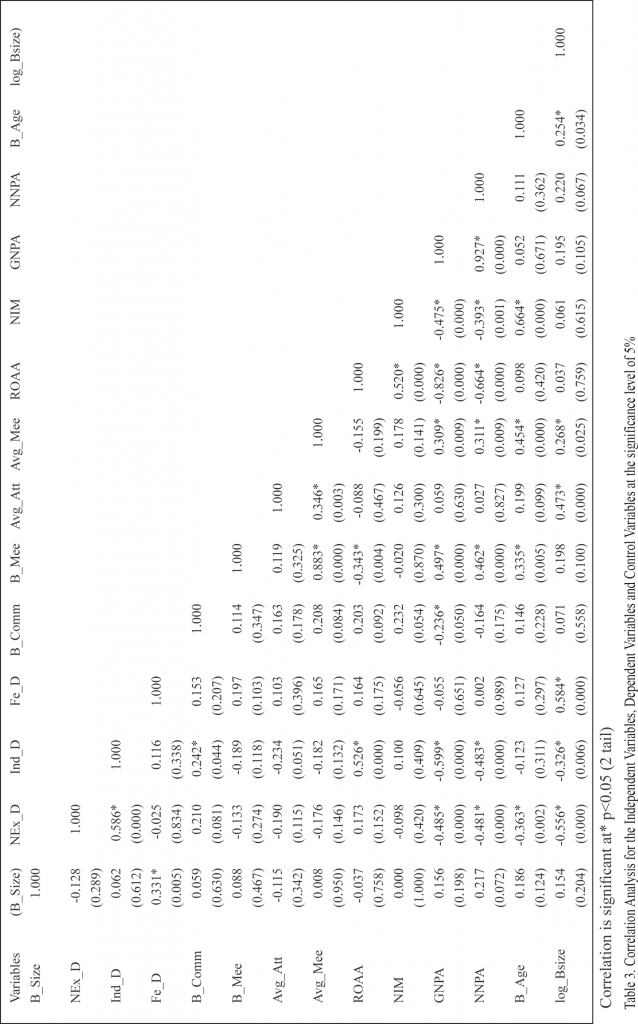

Pearson pairwise correlation method is used to understand the relationship between various variables, which are further explored by using regression analysis. The statis- tical significance of the relationship is analyzed at a 5 percent significance level. From table 3, we can observe that B_Size is negatively correlated with the Fe_D (.005). The NEx_D are positively correlated with Ind_D (.00) and negatively related with the GNPA (.00). Ind_D are positively correlated with B_Comm (.04), ROAA (.00), and negatively correlated with GNPA (.00). B_Comm is negatively correlated with GNPA (.04). B_Mee is positively correlated with Avg_Mee (.00) and GNPA (.00) and nega- tively correlated with ROAA (.003). Avg_Att is positively correlated with Avg_Mee (.003). Avg_Mee is positively correlated with GNPA (.009).

3.2.3 Regression analysis

Return on Average Asset:

Empirical results in table 5 present the relationship between board characteristics and financial performance. It suggests that only 4 out of 8 board characteristics as the independent director’s proportion, female director’s proportion, and the number of board meetings and committees influence return on assets significantly. The p-value of F- statistics is significant at 1%, indicating that the model is a fit. The adjusted R2 shows that selected independent variables in the model account for 71% of the vari- ance in dependent variables.

B_Size displays a negative impact on the performance, although not significant. It can be ascertained that a larger number of directors increases communication costs and delays strategic decisions due to poor coordination. NEx_D and Ind_D are better monitors of the firm. Independent directors have a positive and significant (at a 5% level) impact on performance. The coefficient is .021, which indicates that if there is one unit increase in the proportion of independent directors mean value of ROAA will increase by .021 times, keeping other factors constant. Our finding is in line with (Andres & Vallelado, 2008; Baysinger & Butler, 2019; Garg, 2007; Hermalin & Weis- bach, 1998; Liang et al., 2013). Following the requirements of the “Indian Companies Act, 2013”, “The Securities and Exchange Board of India” (SEBI) made it mandatory for Indian listed companies to have at least one woman director. Both empirical and theoretical studies suggest that female directors are better decision-makers. We find a positive and significant (at 10 percent) relationship between Fe_D and ROAA. The coefficient is 0.025, which indicates that if there is one unit increase in the section of female directors, the mean value of ROAA will increase by .025 times, keeping other factors constant. Our results are consistent with those(Mavrakana & Psillaki, 2019; Pathan & Faff, 2013).

In India, it is mandatory to have at least four board-level committees. Board-level committees help to focus on more strategic and specialized issues. Our results high- light a positive and significant (at a 5% level) relationship between the B_Comm and ROAA supported by Zagorchev & Gao (2015). The coefficient is 0.13, which indi-cates that if there is one unit increase in the number of board committees, the mean value of ROAA will increase by .13 times, keeping other factors constant. Regular board meetings provide a platform to discuss long-term vision, commercial strate- gies, and business transactions. They are one of the greatest ways to ensure that di- rectors can fulfill their responsibilities. But we found a negative association between B-Mee and ROAA, which may be due to the high cost involved in organizing meet- ings supported by (Handa, 2018). The coefficient is -0.21, indicating that if B-Mee is increased by one unit, the mean value of ROAA will decrease by.21 times while all other factors remain constant.

The attendance rate of directors shows diligence toward duties. We use two metrics: the average attendance rate of independent directors and the average attendance rate of board members, both of which are insignificant in terms of financial performance. Control variables such as the age of the bank and the natural log of bank size have a significant relationship (at a 1% level of significance) with the ROAA. Bank age is negatively related, while the size of the bank contributes positively to the bank’s performance. It can be said that a larger bank size helps the bank to reap the benefit of economies of scale.

| Coef. | |

| Chi-square test value | 50.244 |

| P-value | 0 |

Table 4: Hausman specification test (ROAA)

| ROAA | Coef. | St_Err. | t-value | p-value | Sig |

| B_Size | −0.0312059 | 0.0720515 | −0.4331 | 0.6801 | |

| NEx_D | 0.0328006 | 0.0180576 | 1.816 | 0.1192 | |

| Ind_D | 0.0217087 | 0.00781198 | 2.779 | 0.0320 | ** |

| Fe_D | 0.0258626 | 0.0108725 | 2.379 | 0.0549 | * |

| B_Comm | 0.138318 | 0.0516413 | 2.678 | 0.0366 | ** |

| B_Mee | −0.216227 | 0.0815227 | −2.652 | 0.0379 | ** |

| Avg_Att | −2.31075 | 1.84811 | −1.250 | 0.2577 | |

| Avg_Mee | 0.288139 | 0.152332 | 1.892 | 0.1074 | |

| B_Age | −0.297461 | 0.0327927 | −9.071 | 0.0001 | *** |

| log_Bsize | 2.37166 | 0.265675 | 8.927 | 0.0001 | *** |

| Constant | −10.4599 | 1.77543 | −5.892 | 0.0011 | *** |

|

R-squared (Within) F value Prob > F Durbin Watson test Number of obs. |

0.715608 7.3937e+014 1.87041e-044 1.807375 70 |

*** p<.01, ** p<.05, * p<.1

Table 5: Results of the Fixed effect panel data regression (Robust)

Gross non-performing asset

Table 7 indicates the Empirical results of the impact of board characteristics on the asset quality of banks. It shows that 6 out of 8 board characteristics such as NEx_D, Ind_D, Fe_D, B_Comm, B-Mee, and, Avg_Mee influence GNPA significantly. The overall model is fit at a 1% level of significance. The adjusted R2 shows that the 82% percentage of variance in GNPA is reported by selected independent variables in the model. Board size shares a positive relationship with GNPA, which are in line with the findings of (Liang et al., 2013; Sarkar & Sarkar, 2018). Although results are not significant, which keeps the debate open.

The proportion of NEx_D, Ind_D, and Fe_D shares a negative relationship with GNPA. Outside directors don’t participate in day-to-day activities. The coefficient is -0.14, which indicates that if there is one unit increase in NEx_D mean value of GNPA will decrease by -0.14 times, keeping other factors constant. Our results sup- port the hypothesis that there is a significant role in the proportion of independent directors in asset quality (Bezawada, 2020). The coefficient is -0.053, which indi- cates that if there is one unit increase in Ind_D mean value of GNPA will decrease by -0.053 times, keeping other factors constant. Females are considered better at risk management which is also highlighted by our findings. The value of the coefficient is -0.10, which indicates that if there is one unit increase in Fe_D mean value of GNPA will decrease by -0.10 times, keeping other factors constant.

Asset quality has a negative association with B_Comm while a positive association with B_Mee. Both are highly significant at 1% level. Avg_Att shows a significant negative re- lationship at the 1% level, indicating that greater participation leads to better risk man- agement. Related to control variables, bank age displays a significant (at 1 percent level) positive relationship with the GNPA. It is possible that the longer the bank survives in the industry face bureaucratic costs, political interference, and lack of coordination. While the size of the bank is inversely related to GNPA. Perhaps this is due to larger banks become more efficient in handling non-performing loans within the organization.

| Coef. | |

| Chi-square test value | 24.468 |

| P-value | .006 |

Table 6: Hausman specification test (GNPA)

|

ROAA |

Coef. |

St.Err. |

t-value |

p-value |

Sig |

|

B_Size |

0.193334 |

0.272018 |

0.7107 |

0.5039 |

|

|

NEx_D |

−0.144383 |

0.0654871 |

−2.205 |

0.0696 |

* |

|

Ind_D |

−0.0531583 |

0.0205124 |

−2.592 |

0.0411 |

** |

|

Fe_D |

−0.101208 |

0.0436830 |

−2.317 |

0.0597 |

* |

|

B_Comm |

−0.378634 |

0.0962774 |

−3.933 |

0.0077 |

*** |

|

B_Mee |

0.634007 |

0.0943649 |

6.719 |

0.0005 |

*** |

|

Avg_Att |

1.65252 |

2.32822 |

0.7098 |

0.5045 |

|

|

Avg_Mee |

−0.613817 |

0.106713 |

−5.752 |

0.0012 |

*** |

|

B_Age |

0.597747 |

0.272350 |

2.195 |

0.0706 |

* |

|

log_Bsize |

−3.85062 |

3.49005 |

−1.103 |

0.3122 |

|

|

Constant |

28.8453 |

11.5106 |

2.506 |

0.0462 |

** |

|

R-squared |

0.821666 |

|

|

|

|

|

(Within) |

6.81454e+013 |

||||

|

F value |

2.38897e-041 |

||||

|

Prob > F |

1.376204 |

||||

|

Durbin Wat- |

70 |

||||

|

son test |

|

||||

|

Number of |

|

||||

|

obs. |

|

*** p<.01, ** p<.05, * p<.1

Table 7: Results of the Fixed effect panel data regression (Robust)

4. Conclusions and Limitations of the study:

The expanding importance of banks, particularly in emerging economies like India, and the unique role they play in the economy, encourages scholars to look at aspects that influence performance and asset quality. Amid the ongoing reforms (privatiza- tion of public sector banks), discussion on governance reforms, surging scams, and financial crises, this study gives a preliminary overview of the role of board gover- nance. Findings are relevant to the researchers, investors, and regulators as they will learn more about how board dynamics affect financial performance and asset quality. Furthermore, it will guide them to focus on specific board attributes related to private banks, which majorly affect the profitability and quality of assets.

The study employs eight board characteristics, two performance indicators, and two con- trol variables. Financial statements and the CMIE database are used to compile data. The fixed-effects econometrics method is used based on the Hausman test and the LM test. We found that the proportion of independent directors, female directors, board committees, and meetings have a significant impact on the return on assets. Regarding asset quality, along with the above four characteristics, the average no. of meetings attended and non-executive directors have a significant impact on gross non-performing assets.

Because of the small sample size, a more thorough investigation is required to ensure that the findings are generalizable. More studies with other performance measures, a larger time horizon, and larger representative samples are needed to reach reliable findings. Apart from the financial performance, the influence of board governance on other decisions regarding financial matters, such as decisions regarding capital structure and dividend payout can also be researched. The current research might be viewed as a first step toward investigating the consequences of corporate governance in Indian banks, which are typically left out of studies due to their special nature of activities and regulatory system.

Dr. Garima Dalal, Associate Professor, IMSAR, M.D University, Rohtak-124001, Haryana

drgarimadalal@gmail.com, M-9992430000 https://orcid.org/0009-0007-3348-0839

Dr. Sonia, Associate Professor, IMSAR, M.D University, Rohtak-124001, Haryana drsoniaimsar@gmail.com, 9991568177

https://orcid.org/0009-0005-2932-1726

Ishu, Research Scholar, IMSAR, M.D University, Rohtak-124001, Haryana ishu.rs.imsar@mdurohtak.ac.in, 9996373468

https://orcid.org/0000-0002-8277-6077

References:

Abdul Gafoor, C. P., Mariappan, V., & Thyagarajan, S. (2018). Board characteristics and bank performance in India. IIMB Management Review, 30(2), 160–167. https:// doi.org/10.1016/j.iimb.2018.01.007

Adams, Renee B., & Mehran, H. (2003). Is Corporate Governance Different for Bank Holding Companies? SSRN Electronic Journal, 212. https://doi.org/10.2139/ssrn.387561

Adams, Renee B., & Mehran, H. (2005). Corporate Performance, Board Structure, and Their Determinants in the Banking Industry. SSRN Electronic Journal, 212. https://doi.org/10.2139/ssrn.1150266

Adams, Renée B., & Mehran, H. (2012). Bank board structure and performance: Evi- dence for large bank holding companies. Journal of Financial Intermediation, 21(2), 243–267. https://doi.org/10.1016/j.jfi.2011.09.002

Almoneef, A., & Samontaray, D. P. (2019). Corporate governance and firm perfor- mance in the Saudi banking industry. Banks & bank systems, (14, Iss. 1), 147-158.

Andres, P. de, & Vallelado, E. (2008). Corporate governance in banking: The role of the board of directors. Journal of Banking and Finance, 32(12), 2570–2580. https:// doi.org/10.1016/j.jbankfin.2008.05.008

Aqlan, S. A., Lahane, R. B., Farhan, N. H. S., Aswale, S., & Lengare, K. B. (2020). Board characteristics and banks profitability : empirical evidence from India. Studies in Economics and Business Relations, 1(1), 9–20.

Arora, A., & Sharma, C. (2016). Corporate governance and firm performance in de- veloping countries: evidence from India. Corporate Governance (Bingley), 16(2), 420–436. https://doi.org/10.1108/CG-01-2016-0018

Baltagi, B. H., & Song, S. H. (2006). Unbalanced panel data: A survey. Statistical Papers, 47(4), 493–523. https://doi.org/10.1007/s00362-006-0304-0

Battaglia, F., Gallo, A., & Graziano, A. E. (2014). Strong Boards, Risk Commit- tee and Bank Performance: Evidence from India and China. 79–105. https://doi. org/10.1007/978-3-642-44955-0_4

Baysinger, B. D., & Butler, H. N. (2019). Corporate governance and the board of directors: Performance effects of changes in board composition. Corporate Gover- nance: Values, Ethics and Leadership, 1(1), 215–238. https://doi.org/10.1093/oxford- journals.jleo.a036883

Belkhir, M. (2009). Board of directors’ size and performance in the banking in- dustry. International Journal of Managerial Finance, 5(2), 201–221. https://doi. org/10.1108/17439130910947903

Ben Zeineb, G., & Mensi, S. (2018). Corporate governance, risk and efficiency: evi- dence from GCC Islamic banks. Managerial Finance, 44(5), 551–569. https://doi. org/10.1108/MF-05-2017-0186

Berger, A. N., Kick, T., & Schaeck, K. (2014). Executive board composition and bank risk taking. Journal of Corporate Finance, 28, 48–65. https://doi.org/10.1016/j.jcor- pfin.2013.11.006

Bertay, A. C., Demirgüç-Kunt, A., & Huizinga, H. (2013). Do we need big banks? Evidence on performance, strategy and market discipline. Journal of Financial Inter- mediation, 22(4), 532–558. https://doi.org/10.1016/j.jfi.2013.02.002

Bezawada, B. (2020). Corporate Governance Practices and Bank Performance: Evi- dence from Indian Banks. Indian Journal of Finance and Banking, 4(1), 33–41. https://doi.org/10.46281/ijfb.v4i1.502

Bokpin, G. A. (2013). Ownership structure, corporate governance and bank efficiency: An empirical analysis of panel data from the banking industry in Ghana. Corporate Governance (Bingley), 13(3), 274–287. https://doi.org/10.1108/CG-05-2010-0041

Dey, S. K., & Sharma, D. (2021). Nexus between corporate governance and finan- cial performance: Corroboration from Indian Banks. Universal Journal of Accounting and Finance, 8(4), 140–147. https://doi.org/10.13189/UJAF.2020.080406

Dong, Y., Girardone, C., & Kuo, J. M. (2017). Governance, efficiency and risk tak- ing in Chinese banking. British Accounting Review, 49(2), 211–229. https://doi. org/10.1016/j.bar.2016.08.001

El-Masry, A. A., Elbahar, E., & AbdelFattah, T. (2016). Corporate governance and risk management in GCC Banks.

Fama, E. F., & Jensen, M. C. (1983). Separation of ownership and control. The jour- nal of law and Economics, 26(2), 301-325.

Fernandes, C., Farinha, J., Martins, F. V., & Mateus, C. (2016). Determinants of Euro- pean Banks’ Bailouts Following the 2007-2008 Financial Crisis. Journal of Interna- tional Economic Law, 19(3), 707–747. https://doi.org/10.1093/jiel/jgw060

Ferreira, D., Kirchmaier, T., & Metzger, D. (2012). Boards of Banks. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.1620551

Garg, A. K. (2007). Influence of board size and independence on firm per- formance: a study of Indian companies. Vikalpa, 32(3), 39–60. https://doi. org/10.1177/0256090920070304

Gillan, S. L., & Starks, L. T. (2003). Corporate Governance, Corporate Ownership, and the Role of Institutional Investors: A Global Perspective. SSRN Electronic Jour- nal. https://doi.org/10.2139/ssrn.439500

Haan, J. De, & Vlahu, R. (n.d.). CORPORATE GOVERNANCE OF BANKS : A SUR-

VEY. 30(2), 228–277. https://doi.org/10.1111/joes.12101

Handa, R. (2018). Does corporate governance affect financial performance: A study of select Indian banks. Asian Economic and Financial Review, 8(4), 478–486. https:// doi.org/10.18488/journal.aefr.2018.84.478.486

Handa, R. (2020). Board Committees and Financial Performance : Evidence from select Indian Banks. XXXVIII(4), 98–114.

Hermalin, B. E., & Weisbach, M. S. (1998). Endogenously Chosen Boards of Direc- tors and Their Monitoring of the CEO Benjamin E . Hermalin and Michael S . Weis- bach Source : The American Economic Review , Vol . 88 , No . 1 ( Mar ., 1998 ), pp . 96-118 Public. The American Economic Review, 88(1), 96–118.

Hun, M. P. (2011). Practical Guides To Panel Data Modeling : A Step by Step. Public Management and Public Analysis Program, 1–53.

Jadah, H. M., Murugiah, L. A., & Adzis, A. B. A. (2016). The Effect of Board Char- acteristics on Iraqi Banks Performance. International Journal of Academic Research in Accounting, Finance and Management Sciences, 6(4), 205–214. https://doi. org/10.6007/IJARAFMS/v6-i4/2354

Jaswal, P., & Aggarwal, M. (2021). Board Characteristics And Performance Of Banks- Evidence From India. Turkish Journal of Computer and Mathematics Educa- tion, 12(12), 1723–1733.

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of financial economics, 3(4), 305-360.

Kanojia, S., & Priya, S. (2016). Corporate governance in Indian banks post subprime crisis. Journal of Global Business Insights, 1(2), 50–62. https://doi.org/10.5038/2640- 6489.1.2.1007

Laeven, L. (2013). Corporate governance: What’s special about banks? Annual Review of Financial Economics, 5, 63–92. https://doi.org/10.1146/annurev-finan- cial-021113-074421

Lafuente, E., Vaillant, Y., & Vendrell-Herrero, F. (2019). Conformance and perfor- mance roles of bank boards: The connection between non-performing loans and non- performing directorships. European Management Journal, 37(5), 664–673. https:// doi.org/10.1016/j.emj.2019.04.005

Levine, R. (2003). The Corporate Governance of Banks : A Concise Discussion of Concepts and Evidence. Global Corporate Governance Forum, 3, 1–21.

Liang, Q., Xu, P., & Jiraporn, P. (2013). Board characteristics and Chinese bank perfor- mance. Journal of Banking and Finance, 37(8), 2953–2968. https://doi.org/10.1016/j. jbankfin.2013.04.018

Lin, X., & Zhang, Y. (2009). Bank ownership reform and bank performance in Chi- na. Journal of Banking and Finance, 33(1), 20–29. https://doi.org/10.1016/j.jbank- fin.2006.11.022

Macey, J. R., & O’Hara, M. (2003). Solving the corporate governance problems of banks: A proposal. Banking LJ, 120, 326.

Mavrakana, C., & Psillaki, M. (2019). Do board structure and compensation matter for bank stability and bank performance? Evidence from European banks. Munich Personal RePEc Ar- chive, 95776, 83. https://mpra.ub.uni-muenchen.de/95776/1/MPRA_paper_95776.pdf

Mayur, M., & Saravanan, P. (2017). Performance implications of board size, composi- tion and activity: empirical evidence from the Indian banking sector. Corporate Gov- ernance: The International Journal of Business in Society, 17(3), 466–489. https:// doi.org/10.1108/CG-03-2016-0058

Nayak, P. J., Raman, S., Panse, S., Kar, P., Sengupta, J., Vardhan, H., … & Subrama- nian, K. (2014). Report of the committee to review governance of boards of banks in India. Reserve Bank of India, Mumbai, http://rbidocs. rbi. org. in/rdocs/Publication- Report/Pdfs/BCF-090514FR. pdf.

Nyamongo, E. M., & Temesgen, K. (2013). The effect of governance on performance of commercial banks in Kenya: A panel study. Corporate Governance (Bingley), 13(3), 236–248. https://doi.org/10.1108/CG-12-2010-0107

Ondigo, H. (2019). The Moderating Effect of Firm Characteristics on the Relation- ship between Corporate Governance and Financial Performance of Commercial Bank in Kenya. International Journal of Current Science and Multidisciplinary Research.

Pathan, S. (2009). Strong boards, CEO power and bank risk-taking. Journal of Bank- ing and Finance, 33(7), 1340–1350. https://doi.org/10.1016/j.jbankfin.2009.02.001

Pathan, S., & Faff, R. (2013). Does board structure in banks really affect their perfor- mance? Journal of Banking and Finance, 37(5), 1573–1589. https://doi.org/10.1016/j. jbankfin.2012.12.016

Pathan, S., Skully, M., & Wickramanayake, J. (2007). Board size, independence and performance: An analysis of thai banks. Asia-Pacific Financial Markets, 14(3), 211– 227. https://doi.org/10.1007/s10690-007-9060-y

Polovina, N., & Peasnell, K. (2015). The effect of foreign management and board membership on the performance of foreign acquired Turkish banks. International Journal of Managerial Finance, 34(1), 1–5.

Safiullah, M., & Shamsuddin, A. (2019). Risk-adjusted efficiency and corporate gov- ernance: Evidence from Islamic and conventional banks. Journal of Corporate Fi- nance, 55, 105–140. https://doi.org/10.1016/j.jcorpfin.2018.08.009

Sarafidis, V., & Wansbeek, T. (2021). Celebrating 40 years of panel data analysis: Past, present and future. Journal of Econometrics, 220(2), 215–226. https://doi. org/10.1016/j.jeconom.2020.06.001

Sarkar, J., & Sarkar, S. (2018). Bank Ownership , Board Characteristics and Perfor- mance : Evidence from Commercial Banks. International Journal of Financial Stud- ies, OECD 2010, 1–30. https://doi.org/10.3390/ijfs6010017

Tanna, S., Pasiouras, F., & Nnadi, M. (2011). The Effect of Board Size and Composi- tion on the Efficiency of UK Banks. International Journal of the Economics of Busi- ness, 18(3), 441–462. https://doi.org/10.1080/13571516.2011.618617

Zagorchev, A., & Gao, L. (2015). Corporate governance and performance of financial institutions. Journal of Economics and Business, 82, 17–41. https://doi.org/10.1016/j. jeconbus.2015.04.004