Received: 09th December 2022 Review: 28th January 2023 Accepted: 2nd February 2023

Declarations:

Funding: No organization provided funding to the authors for the work submitted.

Conflict of interest: There was never a conflict of interest between authors throughout the research work.

Abstract

Purpose: The purpose of the article is to shed light on the relationship between bank financial performance and financial risk.

Methodology: To obtain synthesized results, 77 publications using secondary data were employed in a multilevel meta-analysis.

Findings: Findings indicate a negative correlation between credit, liquidity risks and banks’ financial performance. A rise in these risks will affect banks’ financial performance. A multi-level meta-analysis reveals a negative association (-0.2023676) between bank financial risk and performance. The influence of moderators, such as macroeconomic conditions, the type of financial risk, and the study region’s selection, is also evident in the relationship between financial risk and financial performance.

Practical Implications: This study adds to the body of knowledge on using multilevel meta-analysis to evaluate the relationship between bank financial risk and performance.

Contribution/Originality: This study adds to the literature on the multilevel meta- analysis by offering more reliable findings to evaluate the association between bank financial risk and performance. The researchers will be able to comprehend the magnitude of the relationship between financial risk and financial performance as a result.

Keywords: Credit Risk, Liquidity Risk, Market Risk, Interest Rate Risk, Financial Performance, Multilevel Meta-analysis, Variance Decomposition.

http://doi.org/10.53908/NMMR.310105

Introduction

Banks play an important role in boosting the performance of an economy by accepting deposits and lending money (PHAN et al., 2020) but at the same time, the banking sector of the world is phenomenally affected by risk (Zeeshan et al., 2021). Among the other types of risks, Financial Risk is significant for banks as it arises when an institution is not capable of generating enough cash flows to meet its financial obligations such as payment of interest or other debt-related obligations. High Financial Risk indicates that an institution is not able to fulfill its financial obligations and has a higher chance to become bankrupt. It is an important agenda for all banking institutions to manage financial risk effectively after knowing the impact that Financial Risk has on the performance of banks. The trade-off between risk and return is well acknowledged – the higher return comes with higher risk (Tafri et al., 2009). Financial Performance is measured by Return on Assets (ROA) and Return on Equity (ROE). ROE and ROA both are indicators of the profitability of a firm. ROA indicates how efficient management is in generating income by using its assets (Shetty and Yadav; 2019) and ROE measures profit per rupee of equity capital (Hossain, M. S and Ahamed, F 2021).

Banking Institutions should be aware of the various risks affecting the Financial Performance of banks. It is an important fact that risk faced by the bank is of great concern for the policymakers (Shetty and Yadav 2019) Financial Performance of banks is influenced by various types of risks like Credit Risk, Liquidity Risk, Market Risk, and Interest Rate Risk.

Credit Risk arises when a loan given by a bank will not be repaid either partially or fully on time (Saleh and Abu Afifa 2020), (Tekalagn Getahun et al., 2015). This type of risk is one of the most significant hazards faced by banks all the time due to its nature of lending money (Al-Husainy & Jadah 2021). Credit Risk is assessed by analyzing the Financial Performance of banks in an attempt to reduce the effect arising from credit defaults (Bhattarai 2016) (Khalid, N 2021). Liquidity Risk arises when the bank fails to settle its liabilities on their due dates (Saeed 2015). Liquidity is an outcome of non-agreement between long-term assets and short-term liabilities (Saleh and Afifa 2020). This risk can create a negative impact on both capital and the bank’s earnings and therefore banks must make funds available to fulfill future potential requests of borrowers at a reasonable price. Market Risk is a risk of losses that arises due to fluctuations in the interest rate and foreign exchange rate since financial instruments are exposed to market price volatility (Mudanya, Muturi 2018). This risk plays a vital role in raising debt burdens and negatively affects the performance of an economy. Interest Rate Risk arises due to a fall in interest income due to a change or movement in interest rate. Interest Rate Risk is measured by the ratio of the difference between the dollar value of liabilities and the dollar value of assets subject to repricing within the same time period to total capital (Tafri et al. 2009).

Literature Review

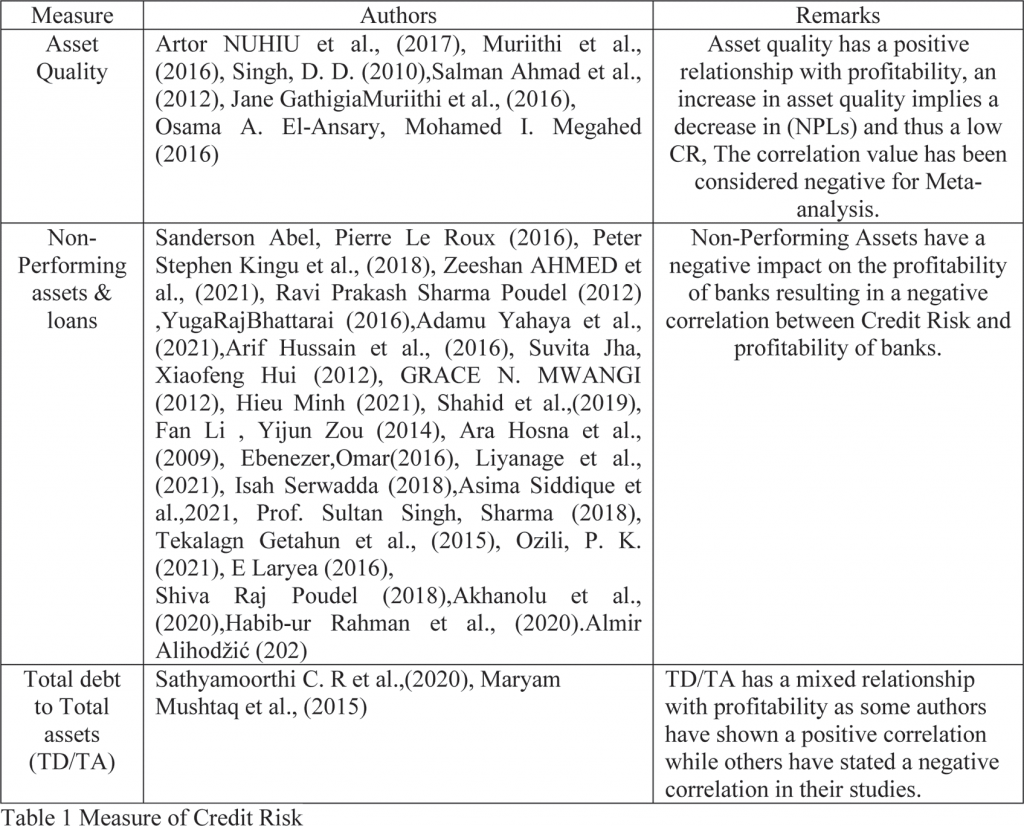

Credit Risk (CR)

Credit Risk is a key factor in determining the performance of the bank. This risk occurs when a creditor or borrower fails to pay its obligation on maturity. Al-Husainy; Jadah (2021), Ghaith N. Al-Eitan et al., (2019), R Ekinci and G Poyraz (2019), all three authors have studied the impact of Credit Risk on the Financial Performance of banks and concluded that Credit Risk has a negative impact on Financial Performance. Yuga Raj Bhattarai., (2016), examined the effect of Credit Risk on the performance of Nepalese commercial Banks and found that these have poor Credit Risk management. Maryam Mushtaq et al., (2015) identified the impact of Credit Risk and capital adequacy on the performance of banks in Pakistan and found that Credit Risk has a negative while capital adequacy has a positive impact on the performance of banks. Peter Stephen Kingu et al., (2018) examined the impact of non-performing loans on bank’s profitability in Tanzania and found that NPL is negatively related to ROA. Khemais Zaghdoudi (2019) identified the effect of different types of risks on the stability of Tunisian conventional banks and found that Credit Risk has no impact on stability. Sanderson Abel and Pierre Le Roux (2016) identified the determinants of profitability of the Zimbabwe banking sector and the results depict that Credit Risk is negatively related with profitability. Ara Hosna et al., (2009) conducted their research on the crisis period and found that after the application of Basel II, the negative impact of Credit Risk on the profitability of banks has increased. Al Karim,

R. and Alam, T. (2013) identified that Credit Risk has negative relation with the performance of banks. Al-Eitan et al., (2021) results of the study revealed that Credit Risk positively affected the performance of the bank. Al-Jafari, M. K and Alchami,

M. (2014) identified that both Credit Risk and Liquidity Risk negatively impacted the profitability of banks in Syria. Alkhatib, A. and Harasheh, M. (2012) results revealed that bank size, credit risk, operational efficiency, and asset management significantly affect banking performance. Çollaku, B. and Aliu, M. (2021) study shows that non- performing loans negatively affected the profitability of banks in Kosovo. Gadzo et al., (2019) identified that both Credit Risk and operational risk have a negative impact on the profitability of banks in Ghana. Jreisat, A. (2020) concluded that Credit Risk negatively affects the Financial Performance of banks due to increasing non- performing loans. Nataraja et al., (2018) in his study found that Credit Risk and bank size were negatively while operational efficiency and asset management were positively correlated with ROE. Hien Thi Kim Nguyen et al., (2018) found a negative relationship between profitability and credit risk (loan loss provision/ total loans)

The Measure of Credit Risk:

Liquidity Risk (LR)

The Measure of Liquidity Risk

Tafri et al., (2009) found that the effect of Interest Rate Risk on ROA was significant while in the case of ROE, Interest Rate Risk was weakly significant for conventional banks. Ratna Barua et al., (2016) found in their study that high-Interest rate reduces the profitability in public sector banks while the effect of high-interest rate was found positive in the case of private banks. Shiva Raj Poudel (2018) results of the study reveal that interest rate has a negative impact on the profitability of banks in Nepal. Habib-ur Rahman et al., (2020) found that interest rate risk reduces the profitability of banks in Pakistan. Zaher Abdel Fattah AL-SLEHAT (2022) found that on the basis of regression analysis interest rate risk has a positive and significant relationship with bank profitability in Jordan.

The Measure of Interest and Market Risk

Risk Management

Raman Ghuman (2018) also examined the impact of Credit Risk management on the Financial Performance of Canara Bank and found that NPA has an inverse relationship with the performance of the bank. Zeeshan AHMED et al., (2021) found that Financial Risk Management has a negative impact on the performance of banks as they considered that Credit Risk, Liquidity Risk, and interest rate risk were important factors of financial risk management. SO Adeusi et al., (2014) and Soyemiet al., (2014) identified the relationship between risk management and Financial Performance in Nigerian banks and reveals that risk management has a significant impact on Financial Performance. Sathyamoorthi C. R et al., (2020) studied the impact of Financial Risk management practices (Credit Risk, Liquidity Risk, and Market Risk) on the Financial Performance of commercial banks in Botswana and found a significant and negative relationship between financial risk management practices and financial performance. Arif Hussain, (2016) studied risk management and bank performance in Pakistan and found better risk management leads to better performance of banks. Akong’a,

C. J. (2014) claimed that there exists a significant impact of risk management on the Financial Performance of banks. Anshika. (2016) in her study concluded that capital adequacy and profitability of banks were affected by the variables like Credit Risk, Liquidity Risk, operating efficiency & inflation rate.

Our Study & Hypothesis development

We aim to investigate the association between Financial Risk and Financial Performance in Banking Industry. We also attempt to examine which moderators influence this relationship. Empirical results are quite different when the positive, negative, and significant relationship is recorded; this divergence in results causes different opinions regarding the direction of the relationship of different Financial Risks on the Financial Performance of banks. The Literature review consists of five categories and for the development of the hypothesis first three categories: Credit Risk, Liquidity Risk, Interest Risk, and Market Risk are considered while the other two categories risk management and bankruptcy prediction are theoretically analyzed. Thus, to find the direction of the relationship, the following hypotheses are proposed

H1: There is a significant relationship between Financial Risk and Financial Performance.

H2: There is a significant impact of region on the relationship between Financial Risk and Financial Performance.

H3: The relationship between Financial Risk and Financial performance is significantly affected by the measure of Financial Risk used.

H4: The relationship between Financial Risk and Financial performance significantly varies by financial crisis period.

H5: The relationship between Financial Risk and Financial performance significantly varies on the basis of panel size.

Inclusion Criteria

All studies available from 2009 to 2022 based on the relationship between Financial Risk and the Financial Performance of banks were included in the current meta- analysis. Several inclusion criteria were framed to select the studies for the purpose of the present study. Firstly, studies had to include the measure of Financial Risk and the measure of Financial Performance and the relationship between them. Secondly, Studies were restricted to the banking sector within the time from 2009-2022. Thirdly, studies only in the English language were considered. Fourthly, only those studies which included sufficient statistical information for calculating effect size and conducting meta-analysis were included. Studies related to bankruptcy predictions of banks were excluded.

Sampling and Methodology

The following search strategy was conducted to arrive at the selected studies. Various E-databases were searched through iisu.refread(Jstor (1966), Ebscohost (226), Indian Journals (1529), Proquest dissertations (3617) & thesis and Shodhganga (2740), Scopus(open access 101) & Dimensions. The search string comprised three elements: Financial Risk measures, Financial Performance measures, and Banking Industry. For Financial Risk measures following keywords were used: (“Financial Risk” OR “Credit Risk” OR “Liquidity Risk” OR “Market Risk” OR “Interest Rate Risk”). For Financial Performance, the following keywords were used: (“Financial Performance” OR “Return on Assets” OR “Return on Equity” OR “Profitability”). To limit the studies to Banking Industry following keywords were used: (“Banks” OR “Banking Sector” OR “Banking” OR “Banking Industry”). Where ever possible, the keywords were mentioned in specific fields i.e the title/abstract/keywords. This enabled us to restrict the number of unqualified studies. In total, 10179 documents were screened. The stepwise screening process as suggested by Pigott and Polanin 2020 was followed. Duplicate citations from different databases were removed. This was followed by abstract screening, methods used, and availability of effect size (R) to exclude the unsuitable studies which did not fit one of the inclusion criteria. This finally led to the Inclusion of 77 numbers of studies for meta-analysis and 161 effect sizes.

Dependent variables:+

Financial Performance (profitability) is taken as the dependent variable and Return on Assets (ROA) and Return on Equity (ROE) are taken as proxies for the measurement of the Financial Performance of banks. ROE measures profitability from the shareholder’s point of view i.e it measures profit per rupee of equity capital Herzuah, A. (2020), Ebrahimi et al., (2021), while ROA determines the ability of the management of a bank to generate profit from assets of banks Aparna Bhatia et al., (2012).

Independent variables:

Financial Risk is taken as the independent variable and different authors have defined Financial Risk in various types such as Credit Risk, Liquidity Risk, Market Risk, and Interest Rate Risk, and all these different risks are taken as proxies for Financial Risk.

Moderators

Moderator Analysis gives the results within Meta Regression framework and enables the investigation of relevant factors which may influence the relation between the variables under study (Harrer, M., Cuijpers, P., Furukawa, T.A., & Ebert, D.D. (2021).

- Region: we have taken region as a potential moderator because the relationship between Financial risk and Financial Performance get influenced by the country of research location, whether the country is developed or developing, the risk-bearing capacity of the country, and monetary measure all these should influence the relationship between FR &

- The Measure of Financial risk: Financial risk is divided into four parts- credit risk, liquidity risk, market risk, and interest rate risk all these risks have different influences on the Financial Performance of

- Macroeconomic variable: Macroeconomic variables e inflation rate and Gross Domestic Product (GDP) of a particular country in which the research was conducted also impact the relationship of Financial Performance with Financial Risk.

- Type of period: Type of period means the time in which the study i.e before or after or during the financial crisis period. The period in which the study was conducted also influenced the relationship between Financial Risk and Financial

- Panel size (n): Panel size = No of years * No of banks. The total panel size taken by the author of the study also influences the relationship between Financial Risk and Financial

- The Measure of financial performance: The two measure of financial performance includes Return on Assets (ROA) and Return on Equity (ROE),both measures of Financial Performance influence the relationship between Financial Risk and Financial Performance.

Data Synthesis: Effect Size Calculation

The methodology suggested by Michael Borenstein, L. V. Hedges, J. P. T. Higgins, and H. R. Rothstein (2009) in the book title Introduction to Meta-Analysis. has been adopted to calculate the effect size. Correlation (r) is converted into Fisher’s z scale and all analyses are performed using transformed values. The transformation is calculated from correlation using the formula:

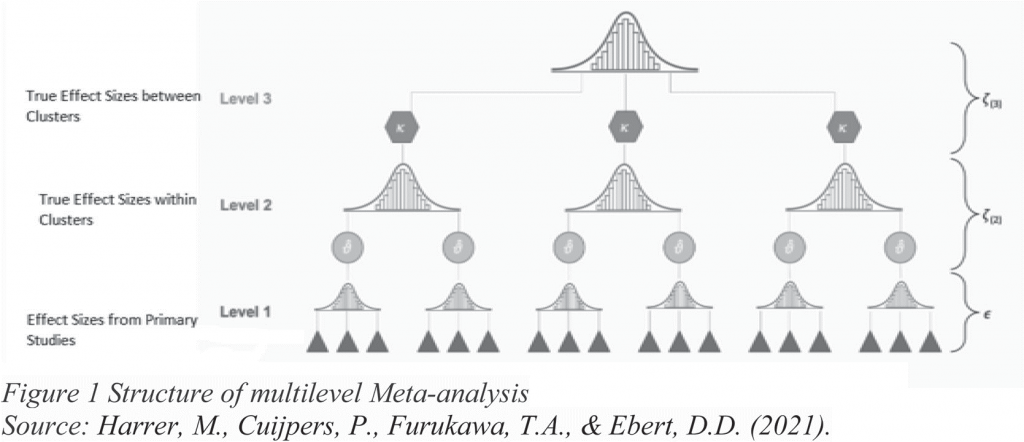

Data Synthesis: Rationale for and Description of the Multilevel Approach

The Methodology suggested by Harrer, M., Cuijpers, P., Furukawa, T.A., & Ebert,

D.D. (2021) in the book title Doing Meta-Analysis with R: A Hands-On Guide has been used for purpose of using multilevel Meta-analysis using R. Multilevel models can more appropriately address multiple ESs within the same study. Three-level model of multi-analysis contains three pooling steps. In the first step, the result of individual participants in primary studies was pooled to report the aggregated effect size. At level 2 the effect sizes are set in within various clusters (k) and these clusters can either be individual studies or can be subgroups of studies. Lastly at the third level overall effect size is obtained by pooling the aggregated cluster effects (u). The formula of the three-level model is:

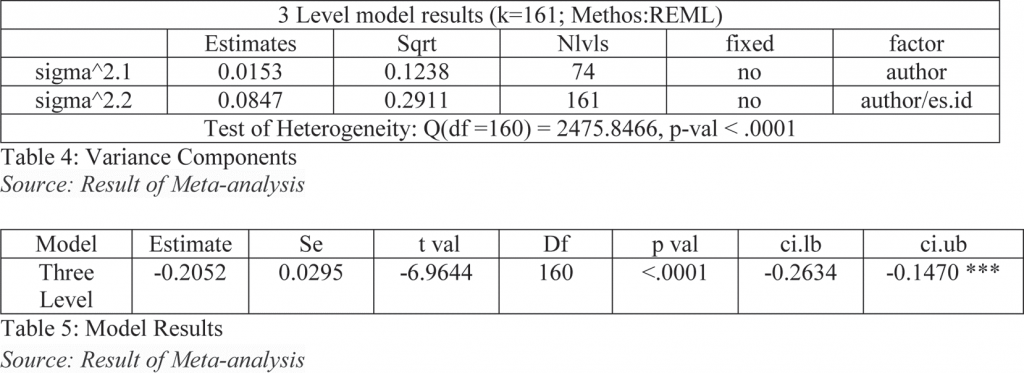

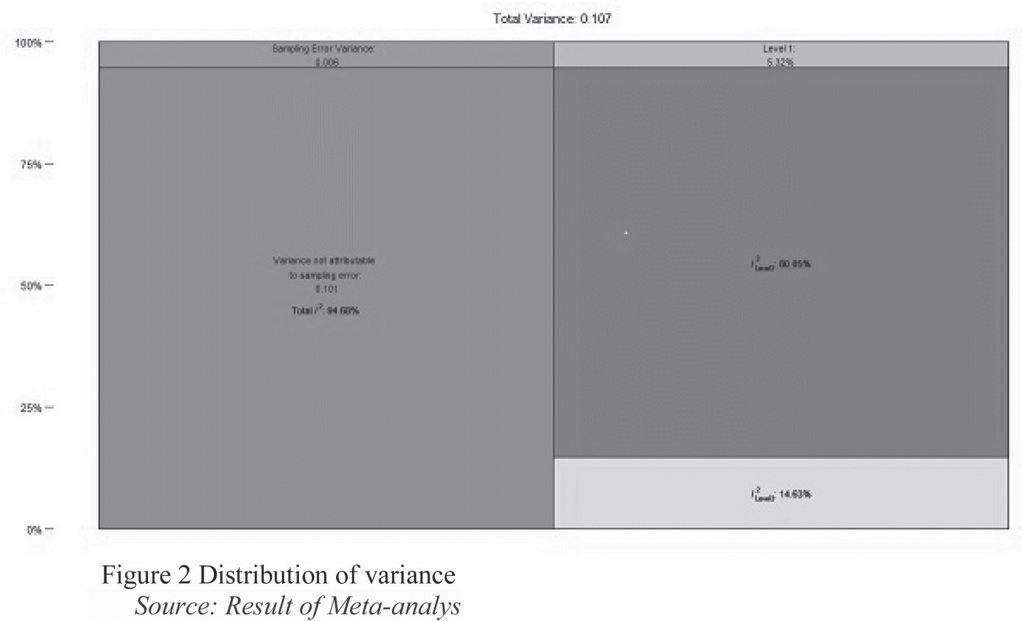

Variance components (Table 4), the random effect variances have been calculated at each level of our model. The first variance component sigma^2.1 denotes level 3 between-cluster variance, this variance in our study is equal to between-study heterogeneity variance τ2 in Meta-analysis (studies are represented by cluster in the model). The second variance component sigma^2.2 denotes the variance within the cluster at level 2. The number of groups on each level is shown in column nlvls, in our study level 3 has 77 groups, equal to k=161 included studies and altogether these 77 studies contain 161 effect sizes. The estimate of our pooled effect (Table 5) is z=

-0.2052 (95%CI: -0.2634–0.1470 ***). To make interpretation easy the effect size is translated back into correlation. The correlation is -0.2023676, which is negative and also not considerably large. This shows that the performance of banks is also affected by various other factors. There seems to be a weak association between Financial Risk and the Financial Performance of banks. The test for heterogeneity in the output points is also significant (p < .0001).

Moderator’s Analysis in Three-Level Models

In the current meta-analysis, we found significant variance both at between and at the within-study level, indicating that the effect size distribution was heterogeneous and that moderating variables may explain differences in the strength of the overall effect size. Moderator analysis shows a significant impact of the moderator region (Europe) country in which the study has been conducted, moderator measure of financial risk (both IRR & LR) i.e the type of risk used, moderator macroeconomic variable which includes Gross Domestic Product (GDP) and Inflation Rate at the time of study and of the country where the study was conducted on the relationship between Financial Risk and Financial performance. Moderators like the type of period, publication year, panel size, Measure of Financial Performance (ROE), and Region (Asia) did not moderate the association between Financial Risk and Financial Performance.

Conclusion

The main objective of this paper is to investigate the relationship between Financial Risk and the Financial Performance of banks. There has been extensive research in the field of Financial Risk in banks and its impact on the Financial Performance of the banks, this research topic got attention after the year 2007 financial crisis that emphasizes the importance to mitigate risks in the banking sector in order to improve their profitability. The review result of 77 papers ranging from 2009-2022 articles reveals that both Credit & Liquidity Risks are the most common measure of Financial Risk and both these risks are negatively associated with the Financial Performance of the banks as an increase in these two types of risk will decrease the performance level of banks. Multilevel Meta-analyses have been used due to multiple effect sizes embedded within an individual research paper. The results of the multi-level Meta- analysis reveal that true effect sizes in terms of correlation between Financial Risk and Financial Performance is -0.2023676 and this is significant at a 95% level of confidence. In addition, the current meta-analytic study provided insights into the effect of moderators on the association between Financial Risk and the Financial Performance of banks. Moderators like Measures of Financial Risk ie Interest Rate Risk (IRR) and Liquidity Risk (LR), Macroeconomic variables like GDP, Inflation and whether the study is conducted in European Countries, significantly moderated the association between Financial Risk and Financial Performance of banks.

Insights for future research:

- The result of the study suggests that meaningful results can be achieved by studying the relationship between Financial Risk and Financial Performance in presence of the micro and macro-economic factors.

- Knowing the risk and studying its impact has no meaning until it is effectively Therefore, further studies may be undertaken to manage the relationship between Financial Risk and Financial Performance.

- Further research may incorporate the impact of Structural breaks such as Covid-19, mergers and acquisitions of banks, and financial scams in banks to better understand the above relationship.

- The Endogenous nature of the measure of Financial Risk (CR, LR, IRR, MR) also needs to be taken into consideration while determining the cause & effect relationship between Financial Risk and Financial Performance because this might give different insights into the relationship between the two

Ms. Harsha Motyani, Research Scholar, Department of Management, IIS (Deemed to be University), 105, Kanwar Nagar, Jaipur, Rajasthan, 302002, India,

Email id: harshamotyani@gmail.com

Orcid id https://orcid.org/0000-0003-4222-5630

Dr. Roopam Kothari, Associate Professor, Department of Management, IIS (Deemed to be University), Gurukul Marg, SFS, Hans Vihar, Kalyanpura, Mansarovar, Jaipur, Rajasthan, 302020, India, Email id: roopam.kothari@iisuniv.ac.in

Orcid id https://orcid.org/0000-0002-5260-3685

Abel, S., & Le Roux, P. (2016). Determinants of banking sector profitability in Zimbabwe. International Journal of Economics and Financial Issues, 6(3).

Adeusi, S. O., Akeke, N. I., Adebisi, O. S., & Oladunjoye, O. (2014). Risk management and Financial Performance of banks in Nigeria. Risk Management, 6(31), 123-129.

Ahmad, S., Nafees, B., & Khan, Z. A. (2012). Determinants of profitability of Pakistani banks: Panel data evidence for the period 2001-2010. Journal of Business Studies Quarterly, 4(1), 149.

AHMED, Z., SHAKOOR, Z., KHAN, M. A., & ULLAH, W. (2021). The Role of

Financial Risk Management in Predicting Financial Performance: A Case Study of Commercial Banks in Pakistan. The Journal of Asian Finance, Economics, and Business, 8(5), 639-648.

Akhanolu, I. A., Ehimare, O. A., Mathias, C. M., Deborah, K. T., & Yvonne, O. K. (2020). The Impact of Credit Risk Management and Macroeconomic Variables on Bank Performance in Nigeria. WSEAS Transactions on Business and Economics, 17, 956-955.

Akong’a, C. J. (2014). The effect of Financial Risk management on the Financial Performance of commercial banks in Kenya (Doctoral dissertation).

Al Karim, R., & Alam, T. (2013). An evaluation of Financial Performance of private commercial banks in Bangladesh: Ratio analysis. Journal of Business Studies Quarterly, 5(2), 65.

Al-Eitan, G. N., & Bani-Khalid, T. O. (2019). Credit Risk and Financial Performance of the Jordanian commercial banks: A panel data analysis. Academy of Accounting and Financial Studies Journal, 23(5), 1-13.

Al-Eitan, G. N., Alkhazaleh, A. M., Alkazali, A. S., & Al-Own, B. (2021). The Internal and External Determinants of the Performance of Jordanian Islamic Banks: A Panel Data Analysis. Asian Economic and Financial Review, 11(8), 644-657.

Alexiou, C., & Sofoklis, V. (2009). Determinants of bank profitability: Evidence from the Greek banking sector. Economic annals, 54(182), 93-118.

Al-Husainy, N. H. M., & Jadah, H. M. (2021). The Effect of Liquidity Risk and Credit Risk on the Bank Performance: Empirical Evidence from Iraq. iRASD Journal of Economics, 3(1), 58-67.

Alihodžić, A. (2020). Sensitivity of bank profitability to changing in certain internal and external variables: the case of Bosnia and Herzegovina. Eastern Journal of European Studies, 11(2).

Ali, B. J., & Oudat, M. S. (2020). Financial Risk and the Financial Performance in listed Commercial and Investment Banks in Bahrain Bourse. International Journal of Innovation, Creativity and Change, 13(12), 160-180.

Alim, W., Ali, A., & Metla, M. R. The Effect of Liquidity Risk Management on

Financial Performance of Commercial Banks in Pakistan. Journal of Applied Economics and Business, 9(4), 109-128.

Al-Jafari, M. K., & Alchami, M. (2014). Determinants of bank profitability: Evidence from Syria. Journal of Applied Finance and Banking, 4(1), 17.

Alkhatib, A., & Harasheh, M. (2012). Financial Performance of Palestinian commercial banks. International Journal of business and social science, 3(3).

Al-Slehat, Z. A. F. (2022). Effect of interest rate risk on financial performance the mediating role of banking security degree: evidence from the financial sector in Jordan. Business: Theory and Practice, 23(1), 165-174.

Anshika. (2016). Impact of Financial Risk management on capital adequacy and profitability- A panel study of selected Indian commercial banks: A quarterly peer reviewed multi-disciplinary international journal. Splint International Journal of Professionals, 3(3), 136-147

Anwen, T. G. L., & Bari, M. S. (2015). Credit Risk Management and Its Impact on Performance of Commercial Banks: In of Case Ethiopia. Research Journal of Finance and Accounting, 6(24), 53-64.

Asllanaj, R. (2018). Does Credit Risk Management affect the Financial Performance of Commercial Banks in Kosovo?. International Journal of Finance & Banking Studies (2147-4486), 7(2), 49-57.

Barua, R., Roy, M., & Raychaudhuri, A. (2016). Structure, conduct and performance analysis of Indian Commercial Banks. South Asian Journal of Macroeconomics and Public

Bhatia, A., Mahajan, P., & Chander, S. (2012). Determinants of profitability of private sector banks in India. Indian Journal of Accounting, 42(2), 39-51.

Bhattarai, Y. R. (2016). Effect of Credit Risk on the performance of Nepalese commercial banks. NRB Economic Review, 28(1), 41-64.

Çollaku, B., & Aliu, M. (2021). Impact of Non-Performing Loans on Bank’s Profitability: Empirical Evidence from Commercial Banks in Kosovo. Journal of Accounting, Finance and Auditing Studies, 7(3), 226-242.

Ebenezer, O. O., & Omar, W. A. W. (2016). The empirical effects of Credit Risk on profitability of commercial banks: Evidence from Nigeria. International Journal of Science and Research, 5(8), 1645-1650.

Ebrahimi, P., Fekete-Farkas, M., Bouzari, P., & Magda, R. (2021). Financial

Performance of Iranian Banks from 2013 to 2019: A Panel Data Approach. Journal of Risk and Financial Management, 14(6), 257.

Ekinci, R., & Poyraz, G. (2019). The effect of Credit Risk on Financial Performance of deposit banks in Turkey. Procedia Computer Science, 158, 979-987.

El-Ansary, O., & Megahed, M. (2016). Determinants of Egyptian Banks Profitability Before and After Financial Crisis. El-Ansary, O. and Megahed, MI (2016). Determinants of Egyptian Banks Profitability before and after Financial Crisis, Corporate Ownership and Control, 14(1), 360-372.

Fatma, S. A. H. R. A. O. U. I., & Riadh, P. E. F. The Relationship between risk man- agement and Financial Performance in Algerian banking sector.

Gadzo, S. G., Kportorgbi, H. K., & Gatsi, J. G. (2019). Credit Risk and operational risk on Financial Performance of universal banks in Ghana: A partial least squared structural equation model (PLS SEM) approach. Cogent Economics & Finance, 7(1), 1589406.

Ghuman, R. IMPACT OF CREDIT RISK MANAGEMENT ON FINANCIAL PER- FORMANCE OF BANKS-A STUDY OF CANARA BANK.

Herzuah, A. (2020). Credit Risk Management and Profitability: A Case of Commer- cial Banks in Ghana (Doctoral dissertation, University of Cape Coast).

Hosna, A., Manzura, B., & Juanjuan, S. (2009). Credit Risk management and profit- ability in commercial banks in Sweden. rapport nr.: Master Degree Project 2009: 36.

Hossain, M. S., & Ahamed, F. (2021). Comprehensive Analysis On Determinants Of Bank Profitability In Bangladesh. arXiv preprint arXiv:2105.14198.

Hossain, T. (2020). Determinants of profitability: A study on manufacturing com- panies listed on the Dhaka stock exchange. Asian Economic and Financial Re- view, 10(12), 1496-1508

Hussain, A., Ihsan, A., & Hussain, J. (2016). Risk management and bank Performance in Pakistan. NUML International Journal of Business & Management, 11(2), 68- 80.

Jha, S., & Hui, X. (2012). A comparison of Financial Performance of commercial banks: A case study of Nepal. African Journal of Business Management, 6(25), 7601- 7611.

Jreisat, A. (2020). Credit Risk, economic growth and profitability of banks. Interna- tional Journal of Economics and Business Research, 20(2), 152-167.

Khalid, M. S., Rashed, M., & Hossain, A. (2019). The Impact of Liquidity Risk on Banking Performance: Evidence from the Emerging Market. Global Journal of Man- agement and Business Research

Khalid, N. An Evaluation of Credit Risk Management and its Impact on the Financial Performance: Evidence from the Banking Sector of Pakistan.

Kingu, P. S., Macha, S., & Gwahula, R. (2018). Impact of non-performing loans on bank’s profitability: Empirical evidence from commercial banks in Tanzania. Inter- national Journal of Scientific Research and Management, 6(1), 71-79.

Laryea, E., Ntow-Gyamfi, M., & Alu, A. A. (2016). Nonperforming loans and bank profitability: evidence from an emerging market. African Journal of Economic and Management Studies

Liyanage, N. H., Dewa, I. S. K., & Ismail, F. I. M. (2021). Credit Risk Management and Bank Performance: With Special Reference to Specialized Banks in Sri Lanka. Asia- Pacific Journal of Management and Technology (AJMT), 2(1), 1-10.

MENGISTU, in Ethiopia M. (2018). The Effect of Credit Risk Management on Profit- ability of Selected Commercial Banks (Doctoral dissertation, St. Mary’s University).

Minh, H. (2021). Analysing Liquidity, Credit Risk and Deposit Money Banks Profit- ability in Nigeria. Turkish Journal of Computer and Mathematics Education (TUR- COMAT), 12(3), 2436-2442.

MUDANYA, L. E., & MUTURI, W. (2018). Effects of Financial Risk on Profitability of Commercial Banks Listed in the Nairobi Securities Exchange. International Jour- nal of Social Sciences Management and Entrepreneurship (IJSSME), 1(1).

Muriithi, J. G., Waweru, K. M., & Muturi, W. M. (2016). Effect of Credit Risk on Financial Performance of commercial banks Kenya.

Mushtaq, M., Ismail, A., & Hanif, R. (2015). Credit Risk, capital adequacy and banks performance: An empirical evidence from Pakistan. International Journal of Financial Management, 5(1), 27-32.

Mwangi, F. M. (2014). The effect of Liquidity Risk management on Financial Perfor- mance of commercial banks in Kenya (Doctoral dissertation, University of Nairobi).

Mwangi, G. N. (2012). The effect of Credit Risk management on the Financial Perfor- mance of commercial banks in Kenya (Doctoral dissertation).

Nataraja, N. S., Chilale, N. R., & Ganesh, L. (2018). Financial Performance of private commercial banks in India: multiple regression analysis. Academy of Accounting and Financial Studies Journal, 22(2), 1-12.

Nguyen, H. T. K., & Nguyen, D. T. (2018). Globalisation and bank performance in Vietnam. Malaysian Journal of Economic Studies, 55(1), 49-70.

Nuhiu, A., Hoti, A., & Bektashi, M. (2017). Determinants of commercial banks prof- itability through analysis of Financial Performance indicators: evidence from Koso- vo. Business: Theory and Practice, 18, 160-170. .

Oudat, M. S., & Ali, B. J. (2021). The Underlying Effect of Risk Management On

Banks’ Financial Performance: An Analytical Study On Commercial and Investment Banking in Bahrain. Ilkogretim Online, 20(5).

Ozili, P. K. (2021). Bank profitability determinants: comparing the united states, Ni- geria and South Africa. Nigeria and South Africa (January 1, 2021).

PHAN, H. T., HOANG, T. N., DINH, L. V., & HOANG, D. N. (2020). The deter-

minants of listed commercial banks’ profitability in Vietnam. The Journal of Asian Finance, Economics, and Business, 7(11), 219-229.

Poudel, R. P. S. (2012). The impact of Credit Risk management on Financial Per- formance of commercial banks in Nepal. International Journal of arts and com- merce, 1(5), 9-15.

Poudel, S. R. (2018). Impact of credit risk on profitability of commercial banks in Nepal. Journal of Applied and Advanced Research, 3(6), 161-170.

Rahman, A., & Saeed, M. H. (2015). An empirical analysis of Liquidity Risk and per- formance in Malaysia Banks. Australian Journal of Basic and Applied Sciences, 9(28), 80-84.

Rahman, H. U., Yousaf, M. W., & Tabassum, N. (2020). Bank-specific and macro- economic determinants of profitability: a revisit of Pakistani banking sector under dynamic panel data approach. International Journal of Financial Studies, 8(3), 42.

Rudhani, L. H., & Balaj, D. (2019). The Effect Of Liquidity Risk on Financial Performance. Advances in Business-Related Scientific Research Journal, 10(1), 20- 31.

Saeed, M. H. (2015). Examining the relationship between operational risk, Credit Risk and Liquidity Risk with performance of Malaysia banks (Doctoral dissertation, Universiti Utara Malaysia).

Saleh, I., & Abu Afifa, M. (2020). The effect of Credit Risk, Liquidity Risk and bank capital on bank profitability: Evidence from an emerging market. Cogent Economics & Finance, 8(1), 1814509.

Sathyamoorthi, C., Mapharing, M., Mphoeng, M., & Dzimiri, M. (2020). Impact of Financial Risk management practices on Financial Performance: Evidence from commercial banks in Botswana. Applied Finance and Accounting, 6(1), 25-39.

Sayani, H., Kishore, P., & Kumar, V. (2017). Internal determinants of return on equity: case of the UAE commercial banks. Banking and Finance Review, 9(1), 47-74.

Serwadda, I. (2018). Impact of Credit Risk management systems on the Financial Performance of commercial banks in Uganda. Acta Universitatis Agriculturae et Silviculturae MendelianaeBrunensis.

Shetty, C., & Yadav, A. S. (2019). Impact of Financial Risks on the Profitability of Commercial Banks in India. management, 7, 550.

Siddique, A., Khan, M. A., & Khan, Z. (2021). The effect of Credit Risk management and bank-specific factors on the Financial Performance of the South Asian commercial banks. Asian Journal of Accounting Research.

Singh, D. D. (2010). Bank specific and macroeconomic determinants of bank profitability: The Indian evidence. Paradigm, 14(1), 53-64.

Singh, S., & Sharma, D. K. (2018). Impact of Credit Risk on profitability: A study of Indian public sector banks. International Journal of Research in Economics and Social Sciences (IJRESS), 8(2),492-498.

Soyemi, K. A., Ogunleye, J. O., & Ashogbon, F. O. (2014). Risk management practices and Financial Performance: evidence from the Nigerian deposit money banks (DMBs). The Business & Management Review, 4(4), 345-354

Tafri, F. H., Hamid, Z., Meera, A. K. M., & Omar, M. A. (2009). The impact of Financial Risks on profitability of Malaysian commercial banks: 1996-2005. International Journal of Social, Human Science and Engineering, 3(6), 268-282.

Yahaya, A., Mahat, F., & Yahya, M. H. (2021). Effect of Liquidity and Credit Risk on Banking Performance: Evidence from Sub Saharan Africa. Journal of Economic Cooperation & Development, 42(2).

Youssef, A., & Samir, O. (2015). A comparative study on the Financial Performance between Islamic and conventional banks: Egypt case. International Journal of Business and Economic Development (IJBED), 3(3).

Zaghdoudi, K. (2019). The Effects of Risks on the Stability of Tunisian Conventional Banks. Asian Economic and Financial Review, 9(3), 389-401.

Zou, Y., & Li, F. (2014). The impact of Credit Risk management on profitability of commercial banks: A study of Europe.

Books:

Harrer, M., Cuijpers, P., Furukawa, T.A., & Ebert, D.D. (2021). Doing Meta-Analysis with R: A Hands-On Guide. Boca Raton, FL and London: Chapman & Hall/CRC Press. ISBN 978-0-367-61007-4.https://bookdown.org/MathiasHarrer/Doing_Meta_ Analysis_in_R/multilevel-ma.html

Borenstein, M., Hedges, L. V., Higgins, J. P., & Rothstein, H. R. (2021). Introduction to meta-analysis. John Wiley & Sons.